ACA Medicaid expansion: Lien on me?

Subscribe to xpostfactoid via box at top right (requires only an email address; you'll get 2-3 emails per week on average)

N.B. 6/19: See second update at bottom: there is a bill in the New Jersey legislature, S3489/A5064, that would ended the pursuit of asset recovery for Medicaid enrollees who are not enrolled in long-term care.

I think it's fairly widely understood (at least by me) that Medicaid picks up the tab for long-term care only when the beneficiary has spent down her assets (if she had any), and that when the spouse of such a beneficiary passes the state can claim remaining assets, such as a house.

What I didn't know, and just learned via New Jersey-based elder lawyer Lauren Marinaro, is that most states can recover assets from any Medicaid recipient over age 55 upon that person's death or the death of his spouse (or any children passing age 21 or blind or disabled). In most states, that's true whether or not the Medicaid enrollee obtained long-term care.

A 1993 federal law required states to recover assets from the estates of recipients of long-term care services under Medicaid. States also have the option of recovering for other Medicaid benefits obtained above age 55. As of 2014, 35 states and D.C. were recovering for other benefits.

The ACA Medicaid expansion complicated the picture. Pre-ACA, Medicaid eligibility generally included an asset test -- as it still does for Aged, Blind and Disabled (ABD) Medicaid. In states that have accepted the ACA expansion, however, Medicaid eligibility is extended to anyone* whose household income is below 139% of the Federal Poverty Level (FPL) -- or $17,236 for a single person in 2019.

There is no asset test for Medicaid eligibility under ACA expansion criteria. But in many states (including New Jersey) anyone over age 55 who qualifies as an "expansion" enrollee (as well as any other Medicaid enrollee) is potentially subject to lien on assets and state recovery after death. In New Jersey, the tab would include total capitated premium paid to a Medicaid managed care organization (MCO) for enrollment in a managed Medicaid health plan. (A 2017 update to NJ asset recovery rules is here.)

So let's say you're 57 and own a home and have some tens of thousands of dollars in savings. You get diagnosed with cancer or have a debilitating heart attack and can no longer work, or can only do part-time contracting work. Your income slips below the Medicaid eligibility threshold, and you enroll. You are then potentially running up a tab, payable upon your death or the death of your spouse, or when your surviving children pass age 21.

There is no such liability for anyone obtaining premium tax credits (and Cost Sharing Reduction subsidies) for private marketplace coverage. For those just beyond the Medicaid eligibility line, a benchmark silver plan enhanced by CSR will cover 94% of the average enrollee's costs at a premium of no more than $60 per month (in some areas a silver plan cheaper than the benchmark is available for less, sometimes far less). For older enrollees with some assets, then, marketplace eligibility may make more sense if they have any flexibility in drawing or reporting income. Per Marinaro:

If someone with assets but no income came to me over 55 for ACA planning I’d tell them to cash in just enough of any IRAs, 401ks and cap gains to put your toe over 138%. Unless you need LTC. Then stay put. NJ ACA Medicaid covers LTC.

— Lauren Marinaro (@lauren_marinaro) June 17, 2019

As the federal government picks up 90% of the cost of Medicaid enrollees rendered eligible by ACA criteria, one might wonder why states would bother to pursue the assets of those enrolled under this match rate. A Nov. 2015 MACPAC issue brief noted that in the wake of ACA enactment, "Connecticut, Colorado, and Washington have made amendments to their Medicaid state plans to eliminate recovery for non-LTSS benefits, and Oregon now only pursues recovery for non-LTSS services if LTSS services were also received."** The report further notes the inequity arguably inherent in subjecting the lowest income ACA beneficiaries to asset recovery while exempting those at higher income levels who are subsidized in the marketplace. It also asks whether asset recovery runs counter the ACA's purpose in determining Medicaid eligibility by income only, without reference to assets.**

One further complication with high financial stakes in Jersey, and perhaps other states (courtesy of Lauren Marinaro): if a person enrolled in Medicaid via ACA criteria (income 29%--138% FPL, no Medicare eligibility) is determined to need long-term care services, the MCO will provide those services and get paid at a much higher capitation rate. From the state's model contract for MCOs effective through June 30, 2018 (p. 792), here is the cost contrast between ordinary adult coverage and various classifications of nursing care:

Moreover, a recent report by the New Jersey Office of the State Auditor found that MCOs often classify an enrollee as in need Managed Long-Term Services and Supports (MLTSS) -- and continue to charge rates for those services when the enrollee opts not to receive them. In a one-year period, the report found, "Enhanced capitation totalling $76.2 million was paid to MCOs for those MLTSS-home-based beneficiaries who opted not to utliize MLTSS services" (p. 5). The report's "conservative" estimate was that that 16% of 17,465 home-based MLTSS beneficiaries, or 2,777, opted not to receive services requiring MLTSS enrollment while the MCO billed at the MLTSS rate. For those without Medicare (and so under age 65), average billing rates were $7,921 per month for home-based care and $9,212 for nursing home care.

Thus, the estates of Medicaid enrollees aged 55-65 could ultimately be dunned for thousands of dollars per per month, regardless of whether the enrollee ever received services billed at those elevated rates.

UPDATE, 6/18 - two, via Twitter:

Minnesota passed legislation to eliminate estate recovery for non LTSS Medicaid recipients. Here’s some background and note that state recovery required for LTSS but a state option for non-LTSS services. https://t.co/dxp4gnxpFK

— LynnBlewett (@LynnBlewett) June 18, 2019

UPDATE 2, 6/18: Turns out there is a bill in the New Jersey legislature, S3489/A5064, introduced Feb. 19, 2019 by Joseph Cryan in the Senate and by Assembly reps Downey, Houghtaling and Huttle, that would limit estate recovery to long-term care. From the bill statement:

Currently, New Jersey’s Medicaid estate recovery program pursues recovery of payments provided through the Medicaid program for all services received on or after the age of 55. Under this bill, the DMAHS would be limited to pursuing recovery for costs associated with nursing facility services, home and community-based services, and hospital and prescription drug services provided concurrently with nursing facility or home and community-based services received on or after the age of 55.

UPDATE 3, 6/20: Kathleen O'Brien, somewhere in the NJ Gannett universe, did a good job covering this issue in 2014, when the ACa Medicaid expansion was new. At that point, about 325-350 Medicaid liens were being filed yearly.

Postscript: Stepping back a day later I have to say: this is a really horrific ACA glitch, potentially affecting a lot of people -- some 12 million people have been enrolled in Medicaid under expansion criteria, and a good number of them must be over 55. I think it's well understood that Medicaid will seek to recoup nursing care costs from an estate after the beneficiary and spouse have died. But to put a lien on ordinary Medicaid enrollment is fundamentally fraudulent -- especially when enrollment in affordable health insurance is mandated by law. The two articles linked to in the note below bring this home in personal narratives. And as for Jersey: I suspect the state could recoup more from Medicaid MCOs fraudulently billing for MLTSS services not delivered than they can from Medicaid expansion enrollees.

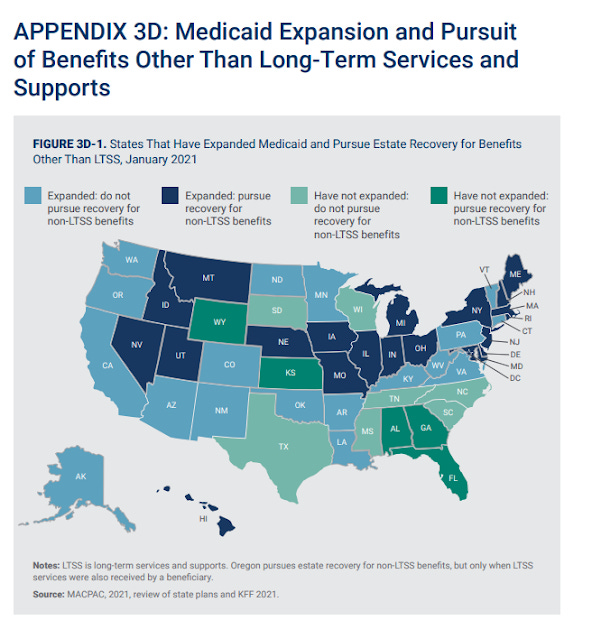

UPDATE 4, 4/7/21: UPDATE 3 (4/7/21) Courtesy of frequent xpostfactoid commenter Bob Hertz: MACPAC's 2021 Report to Congress on Medicaid and CHIP was released in March, and it includes a chapter (3) on Medicaid Estate Recovery. While the report is focused almost exclusively on recovery for LTSS services, it also relays that 20 states and D.C. currently pursue estate recovery for the Medicaid expansion population. It also reveals that estate recovery in all states yielded a grand total of $773 million in 2019. As Bob Hertz puts it, "This is barely a raised dimple in the overall Medicaid program and not worth the fear and torment that is caused." LTSS recoveries in New Jersey were $13.8 million in 2019 and ranged from $12.2 million to $18.6 million from 2015-2019. The map below is from pdf page 47 (report pg. 117) of the MACPAC report.

---

* Anyone, that is, except legally present noncitizens subject to a federal "5-year bar" to Medicaid enrollment, or even longer waiting periods imposed by some states. Those who are time-barred from Medicaid are eligible for ACA marketplace subsidies even if their income is in Medicaid range (0-138% FPL) -- in which case they pay 2% of income for a benchmark silver plan, enhanced by CSR to an actuarial value of 94%. Undocumented immigrants are not eligible for full Medicaid coverage or marketplace subsidies.

** The MACPAC brief also notes several media stories in 2014 and 2015 about the liens, including this from KHN and this from the WSJ. This is not new, just new to me (and I suspect to a lot of people).