For Whom the Bronze Bell Tolls in the ACA Marketplace

My last post looked at the likely impact of the availability of free or very cheap bronze plans for ACA marketplace customers who are eligible for strong Cost Sharing Reduction (CSR), available only with silver plans, in the five largest markets in the country.

In this post, we'll look at current CSR takeup in the five counties in question and consider how it's likely to change. Here are the counties, with their 2017 initial marketplace enrollment totals:

Miami-Dade, FL 387,848

Los Angeles, CA 380,520

Broward, FL 240,984

Harris, TX (Houston) 240,064

Cook, IL (Chicago) 144,418

While bronze plans generally have deductibles above $6,000, CSR-enhanced silver plans, for enrollees with incomes up to twice the Federal Poverty Level, generally have deductibles in the $0-1,000 range. Silver plan premiums can be hard for CSR-eligible buyers to afford, though. The wider the spread between cheapest bronze and cheapest silver premiums, the more people will choose bronze.

This year, the spreads have widened dramatically, so CSR takeup is likely to drop, particularly at the higher CSR-eligible income levels, where silver is relatively more expensive. In three of the five counties in question, and parts of a fourth (Los Angeles), free bronze is available to 40 year-old buyers with incomes just below 200% FPL, the threshold for strong CSR. In Cook County, IL (including Chicago), bronze is $20 per month at that age and income level, vs. $118 for cheapest silver.

CSR takeup has generally been above 80% for enrollees with incomes up to 200% FPL. In the five counties in question, which together account for about 11% of ACA marketplace enrollment, it's above 80% this year for all CSR eligibles taken together.

CSR Takeup in U.S. Counties with Highest Marketplace Enrollment (2017)

County Total Enrolled Total Enrolled at 100-250% FPL CSR enrollment CSR takeup* Miami-Dade 387,848 350,359 298,015 85% Los Angeles 380,520 255,420 207,710 81% Broward 240,984 203,511 176,809 84% Harris 240,064 188,816 157,868 81% Cook 144,418 87,633 73,581 84% Total 1,393,834 1,085,739 913,983 84%

* About 2% of enrollees with CSR have incomes under 100% FPL, a population that HHS did not break out this year. Conversely, though, 1-2% of enrollees in the 100-250% FPL income range are not eligible for CSR. The CSR takeup rates cited here may be about 1% too high.

CSR takeup is high, but it falls as income rises. That's natural, because CSR weakens as income rises, while the percentage of income required to buy the benchmark (second cheapest) silver plan also rises. CSR raises the actuarial value of a silver plan from a baseline of 70% (silver without CSR) to 94% for enrollees with incomes up to 150% FPL, to 87% for enrollees with incomes ranging from 151-200% FPL, and to just 73% for those with incomes between 201-250% FPL. Here are 2017 CSR takeup rates at the three levels of CSR in the 38 states using HealthCare.gov:

Metal Level Selections at Different CSR-eligible Income Levels (% FPL)HealthCare.gov states, 2017

Strong CSR Weak CSR

Metal level 100-150% 151-200% 201-250% bronze 9.2% 14.4% 27.1% silver 89.4% 83.2% 67.6% gold < 1% 1-2% 4-5%

In 2018, silver plan selection is likely to fall off in the middle range of CSR eligibility, where it's historically been quite high. It should fall even more steeply in the highest eligible bracket (201-250% FPL), where CSR is negligible and this year gold plans are in many cases either close to silver in price or actually cheaper.

Here is what the bronze-vs.-silver choice looks like in 2018 for a single 40 year-old at various incomes in Miami-Dade and Broward counties, which together account for 5% of all ACA enrollment. The choice is broadly similar in all five counties considered here, except in large swaths of Los Angeles, where the cheapest bronze plan is $48 per month..

Miami-Dade 33012: Cheapest Bronze, Silver and Gold plans for 40 year-old

Income Cheapest bronze premium (60% AV) Cheapest silver premium Cheapest gold premium (80% AV) $16,000 (133% FPL) $ 0 $ 19 (94% AV) $ 40 $18,000 (149% FPL) $ 0 $ 52 (94% AV) $ 73 $24,000 (199% FPL) $ 0 $118 (87% AV) $139 $30,000 (249% FPL) $56 $194 (73% AV) $215

At bottom, I've pasted more comprehensive plan comparisons from hc.gov for three income levels: just over 100% FPL, just under 200% FPL, and just over 200% FPL

Bronze, I suspect, is going to start to look very tempting at incomes over 150% FPL, and to a lesser extent in the 138-150% FPL band, where the premium for benchmark silver is 3-4% of income, as opposed to just 2% for those in the 100-138% FPL range. In the 201-250% bracket, gold, at 80% AV, may outdraw silver, at 73% AV, while bronze may also draw many.

Now let's look at the incomes at which CSR-eligible enrollees are concentrated in these counties. Florida and Texas refused to implement the ACA Medicaid expansion, and consequently, eligibility for marketplace subsidies starts there at 100% FPL, as opposed to 138% FPL in the expansion states, e.g., California and Illinois. Needless to say, silver plans are most affordable for those in the "should have been in Medicaid" 100-138% FPL band -- and there's a lot of them. Unfortunately, this year HHS did not break out the 100-138% FPL cohort separately, so 100-150% FPL is shown below, As noted in the prior post, though, in 2016 46% of enrollees in Florida and 34% in Texas had incomes between 100-138% FPL.

Silver Enrollment in 100-250% FPL Range by Income Level (2017)

County 100-150% FPL94% AV silver 151-200% FPL 87% AV silver 201-250% FPL73% AV silver Miami-Dade 75% 18% 7% Los Angeles 36% 48% 16% Broward 68% 21% 10% Harris 59% 26% 15% Cook 30% 45% 26% CSR takeup rate - all hc.gov states 89% 83% 68%

To think in Republican terms for a moment, a person earning $24k who might in a previous year have ponied up $118 per month for high-AV silver could theoretically buy a free bronze HSA-linked plan, and put the saved premium toward medical expenses. No one is going to do that. More mundanely, a lot of prospective enrollees can now get a rough equivalent of the subsidy value of strong CSR in a bronze plan -- as perhaps they should always have been able to do. This, however, is an inefficient and convoluted way to do it.

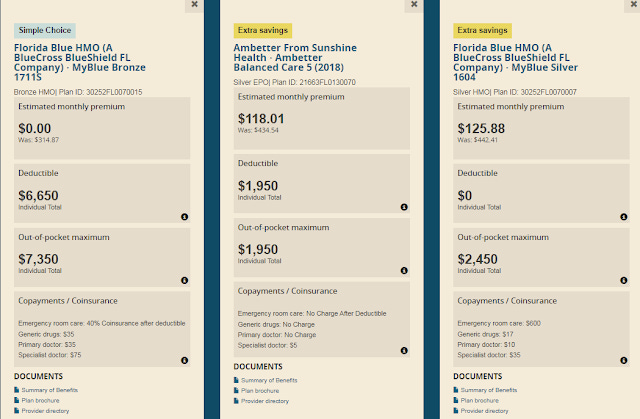

Appendix: The choice at three income levels in Miami-Dade (zip 33012)

Income $12,000, 40 year-old

Income $24,000, 40 year-old

Income $25,000, 40 year-old

Prequel: Free bronze or CSR-boosted silver? The choice in 5 top marketplace countie