Free silver plans at incomes above 150% FPL

The American Rescue Plan enacted last month radically though temporarily boosted premiums in the ACA marketplace. The premium paid by enrollees for the benchmark (second cheapest) silver plan is now set at $0 for enrollees with household incomes up to 150% of the Federal Poverty Level, and at 0-2% of income for enrollees with incomes in the 150-200% FPL range. That tops out at $43 per month for a single person with an income of $25,520.

Bronze plans are now available at zero premium to almost any enrollee with an income below 200% FPL (and to a fair number at higher incomes). But bronze plan deductibles average $6,921. At incomes up to 200% FPL, silver plans come with strong Cost Sharing Reduction (CSR), which brings deductibles down to an average of $177 for enrollees with incomes up to 150% FPL and $800 in the 150-200% FPL range. The contrast is similarly dramatic in annual out-of-pocket maximums, which usually top $8,000 in bronze plans. CSR brings them down to an average of $1189 at incomes up to 150% FPL and $2529 at 150-200% FPL.

Prior to the subsidy boost, increasing numbers of enrollees with incomes below 200% FPL were selecting bronze plans, especially in the 150-200% FPL range, where benchmark silver topped out at $135/month for an individual (see The darker side of free bronze). The newly enhanced subsidies should reverse that trend. Still, even modest premiums are often experienced as steep at low incomes, and zero-premium plans remove administrative friction that deters some enrollees (arranging and executing on monthly premium payment can be surprisingly difficult).

In areas where the cheapest silver plan is significantly cheaper than the benchmark (second cheapest ) silver plan, CSR can be had at a discount. Spreads between cheapest and benchmark silver tend to be pretty narrow, though. Often, one insurer dominates the lower price points, if not the whole market, and it's at that insurer's discretion whether to create a sizeable spread. More often than not, the insurance doesn't. That said, the availability of free silver plans varies by rating area. The spread also widens with age, as premiums rise with age.

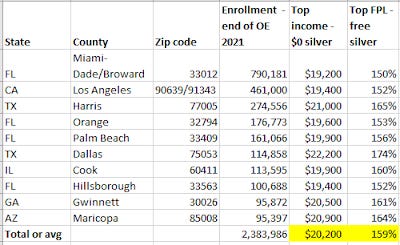

Below, I've charted the income level to which free silver plans are currently available to a 40 year-old in the ten U.S. counties with the highest enrollment, collectively representing 20% of 2021 enrollment. The thresholds would be higher for older enrollees: the premium for a 58 year-old is about twice that paid by a 40 year-old, and the spread between cheapest and benchmark silver rises proportionately. At age 40, the average spread is pretty modest, though not negligible.

Income thresholds for zero-premium silver plans under the American Rescue Plan

40 year-old single enrollee

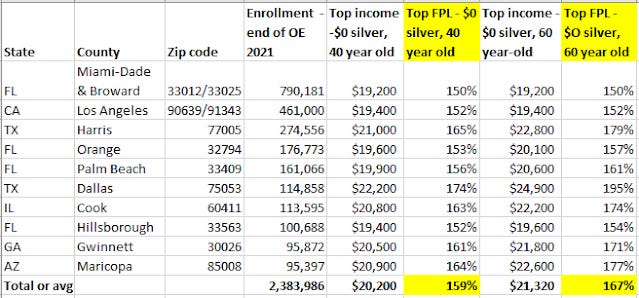

UPDATE: I've added the $0 premium silver thresholds for a 60 year-old below -- on average, $1120 per year higher than for 40 year-olds.

Income thresholds for zero-premium silver plans under the American Rescue Plan

40 year-old and 60 year-old single enrollee

Sources: CMS county-level public use files; HealthSherpa; Covered California Active Member Profiles

The largest counties may not be representative of the whole market. In smaller markets with less competition, a dominant insurer may have more control over spreads. In some cases, monopoly insurers have created large spreads between cheapest and benchmark silver, generating free silver plans before the American Rescue Plan dropped enrollees' premiums overall. Generally, though, silver spreads are modest, as reflected above.

---

A few technical notes: Income levels are rounded to the nearest $100; the availability of $0 premium comes via HealthSherpa's cost estimator, which allows for easy data edits without resetting. I've combined Miami-Dade and Broward counties, because in multiple zip code checks (over several years) their offerings appear to be the same. Conversely, California splits Los Angeles into two rating areas, but this year the pricing appears to be the same across both, at least in the zip codes I checked. In California and Illinois, there are no $0 premium plans; thresholds are for $1/month premiums. Finally, Los Angeles enrollment by county is available only through 2020, in quarterly "active member profiles." I estimated the total for 2021 by multiplying the March 2020 total by the statewide increase from 2020 to 2021, and then, since the totals for the other counties are as of the end of Open Enrollment, boosting the 2020 total by another 4%, as end-of-OE enrollment was 104% of the March active member total (which reflects monthly attrition).