If Democrats get skimpy with ACA enhancement, who should get half a loaf?

With a 50-50 Senate under Democratic control, how far will the Democrats go in rendering health insurance more affordable for those who currently find it unaffordable?

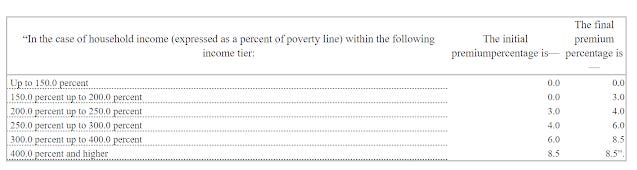

The Affordable Care Enhancement Act passed by the Democratic House last June would reduce the percentage of income paid for a benchmark silver plan in the ACA marketplace at every income level -- and remove the income cap on subsidy eligibility, currently 400% of the Federal Poverty Level ($51,040 for an individual, $104,800 for a family of four). Premiums for a benchmark silver plan would range from $0 (at incomes up to 150% FPL) to 8.5% of income. Here's the scale established by the bill:

And here is the current scale:

Past performance of Democratic majorities breeds some skepticism as to whether a razor-thin Democratic majority would go as far in bolstering subsidies as the ACEA -- let alone implement a strong "Medicare-like" public option as proposed by Biden during the nomination contest (then again, with Bernie Sanders as Senate Budget chair, who knows, maybe they'll go further).

On Twitter yesterday, some healthcare types slipped into playing a kind of Hunger Games: if Dems go for half a loaf, should they concentrate new benefits on those already eligible for subsidies, or on those currently ineligible?

The need is pretty compelling on both sides of the 400% FPL divide. Consider:

Among the subsidy-eligible, takeup of marketplace coverage is below 50%, according to the Kaiser Family Foundation ( or maybe a few points higher than Kaiser calculates).

Enrollment among the unsubsidized in ACA-compliant plans dropped by 2.8 million, or 45%, from 2016 to 2019, according to CMS. That was in the wake of premium increases exceeding 20% in 2017 (a market correction after initial underpricing) and 2018 (driven by the failed Republican repeal drive and regulatory assault).

On one side of this question was Stan Dorn of Families USA, who has been pushing states to improve affordability at lower incomes (up to 300% FPL) for years. The main arguments: uninsured rates are much higher at lower incomes than over 400% FPL; takeup at incomes below 300% FPL in Massachusetts, where coverage is way more affordable than in other states thanks to a Medicaid-like marketplace available up to that threshold, is the best in the nation; and high takeup among the healthy young at lower incomes will drive down unsubsidized premiums (see again Massachusetts, which has the lowest or second lowest premiums in the nation). I would add that according to Kaiser's numbers, about 9-10 million uninsured are eligible for ACA subsidies.

On the other side of the question, tentatively and equivocally, is me. Point one is political: the Affordable Care Act has failed to make coverage affordable for millions of unsubsidized prospective enrollees, and Democrats have been flayed for that since the law's passage -- with some justification. The one subset of Americans that the ACA materially harmed were healthy pre-ACA individual market enrollees who paid less for coverage they found adequately comprehensive -- often far less -- than they had to pay once the ACA marketplace launched (along with their unsubsidized successors). Unquestionably, unsubsidized ACA-compliant coverage is a heavy financial lift, and quite literally unaffordable in some markets. As mentioned above, about 3 million enrollees have been priced out since 2016, and perhaps as many between the ACA marketplace's launch in 2014 and 2016.

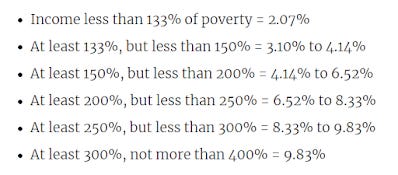

In 2015 -- before the premium surges of 2017-2018 -- Urban Institute scholars Linda Blumberg and John Holahan calculated that individual market enrollees in the 400-500% FPL income bracket paid a higher percentage of income for coverage than any other income group (this in a study that proposed the premium subsidy boosts similar to those incorporated in the ACEA):

In short, both subsidy-eligible and unsubsidized individual market enrollees need more affordable coverage. The most cost-effective way to improve coverage would be to replace the commercial individual market with a public program structured something like Medicare, Medicaid, or Tricare. That seems unlikely. The fear is that by a kind of Murphy's Law of progressive politics, Democrats will neither subsidize to ACEA levels, nor focus fire at a target income group, but pass watered-down subsidy boosts across the board. That's more or less what California has done, with a pretty modest impact on enrollment (Charles Gaba takes a deeper dive into California's subsidies and their effect here).

One further point with regard to concentrating new spending. In addition to pitching states to concentrate supplemental marketplace subsidies at low incomes, Stan Dorn (with Families USA executive director Frederick Isasi) has also proposed a raft of regulatory measures to improve affordability and ease of enrollment. These include CMS mandating full silver loading* so that every prospective marketplace enrollee has access to a gold plan costing less than the benchmark silver plan, and changing the basis by which the actuarial value** of the ACA metal levels is calculated by excluding the most expensive enrollees from the calculation, raising effective AV at each metal level. Taken together, those measures would ensure that every prospective enrollee would have access to coverage at least comparable to average employer-sponsored plans (about 85% AV) for less than the percentage of income required for a benchmark silver plan. Out-of-pocket costs would also shrink for low income enrollees in silver plans enhanced with strong CSR. Combine those measures with legislation capping benchmark premiums at 8.5% of income as in the ACEA and you're a long way toward affordable coverage for all comers.

Of course, the regulatory measures aren't free: they would raise the cost of federal subsidies substantially. But aggressive regulatory action would take some of the heavy financial lift off the shoulders of a barely-Democratic Congress.

---

* Silver loading is a practice first implemented in the ACA marketplace for plans effective in 2018, after Trump cut off direct reimbursement of insurers for Cost Sharing Reduction (CSR) subsidies in October 2017. Since CSR is available only with silver plans, after the cutoff insurers were allowed to price the benefit into silver plan premiums only, which created steep discounts in bronze and gold plans in many states and regions. Silver loading has boosted enrollment, but its implementation has been haphazard and incomplete, as silver plans remain underpriced on average. Regulators can mandate that insurers price silver plans in accordance with their real actuarial value, as the ACA statute in fact requires.

** Actuarial value denotes the percentage of medical costs the average enrollee must pay out pocket, as calculated by a formula provided by CMS. At present, enrollees who exceed the annual out-of-pocket cost limit (about $8,500 this year) skew the average, as Bill Gates walking into a bar would skew the average income of customers present. A bronze plan with an AV of 60% might have a $7,000 deductible and cover just 50% of the cost of most services after the deductible is reached.

Update, 1/19/21: See Charles Gaba's deep dive into various Democratic plans to enhance the ACA on both federal and state levels.

Subscribe to xpostfactoid